Every few months, a new report lands celebrating the subscription model as the salvation of journalism. A newspaper in Scandinavia has cracked it. A digital-first outlet in the US has hit a million paid subscribers. The playbook, we are told, is clear: build trust, produce quality journalism, ask readers to pay for it. The rest will follow.

In India, that playbook lands differently. With 886 million internet users, a media industry worth over 29 billion dollars, and more daily newspapers than almost any country on earth, India looks like fertile ground for reader-funded journalism. But out of those 886 million users, roughly 1.5 million pay for any form of digital news. That is less than 0.2 percent.

This is not a failure of journalism. It is a consequence of a system built, over decades, around a very different set of assumptions about who pays and why. Understanding those assumptions is not just useful for India. It is a window into a problem that many journalism markets are quietly heading toward, regardless of where they are starting from.

Sources: FICCI-EY 2024, EY Media Report 2023, CASI/Barkha Dutt analysis, Reporters Without Borders 2024

The System That Built Itself Around Advertising

India’s news industry was never designed for reader revenue. For most of the post-independence era, newspaper subscription prices were kept deliberately low, sometimes below the cost of production, to maximise circulation and therefore advertising rates. The logic was straightforward: reach as many readers as possible, then sell that reach to advertisers. The reader was never the customer. The reader was the product.

That model worked, in a fashion, for decades. But it created a structural dependency that is now deeply embedded. Today, most Indian news organisations generate close to 90 percent of their revenue from advertising. Corporate advertisers provide the bulk of it. Government advertising provides a significant share on top of that. According to an analysis presented at the Center for Advanced Study of India, the Indian government spent close to one billion dollars on media advertising across print, television and digital platforms in just the last three years. Remove that government spending, and a significant portion of India’s smaller regional news outlets would not survive.

The implications for editorial independence are real and well-documented. When government advertising is a newsroom’s primary lifeline, the incentive to hold that government accountable is structurally compromised. This is not a new observation, but it bears repeating in the context of business models: the problem of press freedom in India and the problem of sustainable local news are not separate issues. They are the same issue, expressed differently.

What Actually Pays for Indian News Today

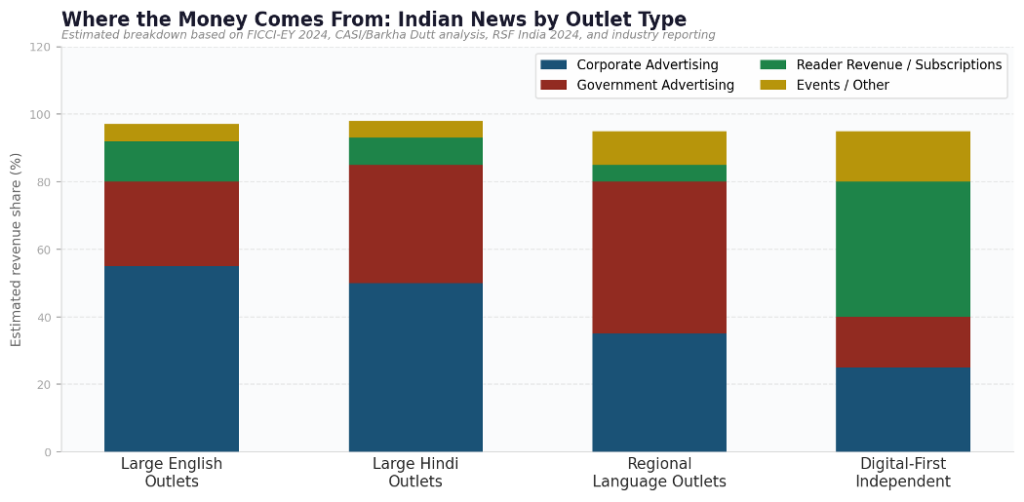

The revenue picture varies significantly by outlet type, but the pattern is consistent: advertising dominates, reader revenue is minimal, and the gap between large national outlets and regional ones is wide.

Estimated revenue share by outlet type. Sources: FICCI-EY 2024, RSF India 2024, CASI analysis, industry reporting

Large English-language outlets have the most diversified revenue, with some meaningful reader revenue and events income supplementing advertising. Hindi-language outlets remain heavily advertising-dependent, with government advertising playing a particularly significant role. Regional language outlets are the most exposed: high government advertising dependence, minimal reader revenue, and the fewest alternative options. Digital-first independents are the outliers, with some having built meaningful reader bases through memberships and donations. But they remain small, and their model has not yet scaled.

The Subscription Gap

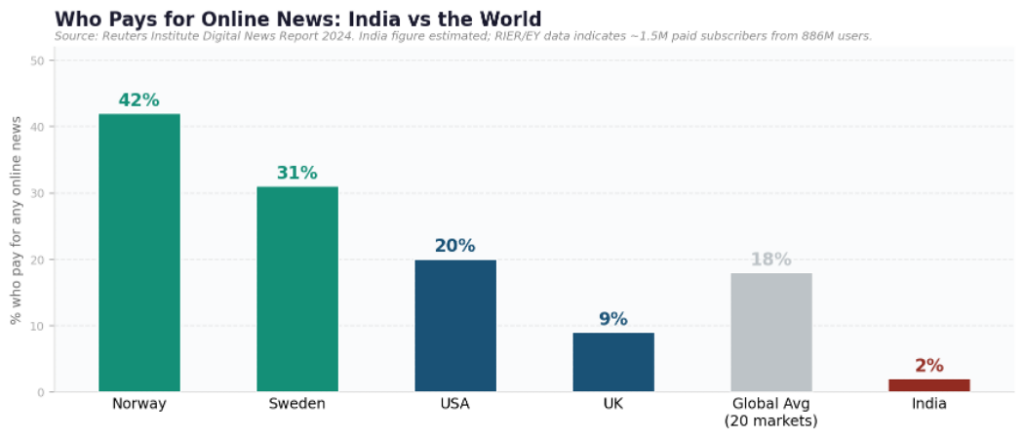

Set India’s situation against the global picture and the scale of the gap becomes clear.

Source: Reuters Institute Digital News Report 2024. India estimate based on EY 2023 data

(1.5M paid subscribers from 886M users)

Norway and Sweden, the markets most often held up as models, have 42 and 31 percent paying rates respectively. The US sits at 20 percent. The global average across 20 markets is 18 percent. India is estimated at under 2 percent, and even that may be generous given that most estimates count e-paper subscribers from print households rather than genuinely new digital paying readers.

The standard explanation for this gap is price sensitivity. India is a developing market, the argument goes. People cannot afford to pay. But Indians pay for streaming video, mobile data, WhatsApp Business subscriptions, and entertainment content at scale. The issue is that readers have never been taught to see news as something worth paying for, because the industry spent decades making it free and subsidising it through advertising.

The Habit We Never Built

Working at the intersection of journalism, technology and content in India, the pattern I keep coming back to is this. The conversation about sustainable news revenue almost always happens in English. And it almost always ends at the same place. English is where the money is. Everything else is a cost to be managed.

Even within regional journalism, there is a hierarchy. Hindi gets the most investment and the most advertiser attention because it has the largest single-language audience. Every other language sits further down. Telugu, Kannada, Tamil, Marathi, Bengali: each with tens of millions of readers, each treated as a secondary market that will be prioritised eventually, once the English and Hindi products are stable.

But the deeper problem is not the language hierarchy. It is that across all of Indian journalism, readers were never asked to value journalism enough to pay for it. And because the advertising model kept the lights on, newsrooms never had to ask that question seriously. The result is that when advertising weakens, when government ad budgets shift, when platforms change their algorithms, there is no reader base to fall back on. The floor collapses.

This is where the comparison with other markets becomes genuinely instructive. The US and UK are dealing with declining advertising revenue and trying to build reader revenue models late in the game. India has not yet even started that transition in any serious way. The question is not whether India will face a local news sustainability crisis. It is whether the industry will act before that crisis arrives, or after.

What Is Actually Working

Amid the structural problems, some things are working. They are worth paying attention to, not because they are perfect, but because they point toward what is possible.

Digital-first independent outlets that have built membership models have found that readers will pay, when they believe the journalism is genuinely independent and genuinely for them. Outlets that combine free access with optional membership, are transparent about their funding, and actively communicate their editorial independence have built loyal paying audiences. These are small in absolute terms. But the conversion rates suggest the appetite exists.

Regional language content is proving its commercial value in adjacent sectors. Streaming platforms that invested in regional language content have seen strong engagement and subscription growth from Tier 2 and Tier 3 markets. Over-the-top content in regional languages accounted for 50 percent of total streaming content consumed in India by 2022, according to PwC research. The audience for paid regional content exists. Journalism has simply not found a way to tap it yet.

Events and community models are emerging quietly. Journalism outlets that have moved beyond content to build genuine communities, through events, forums, and niche memberships, are finding revenue that advertising alone could never provide. The model is not new globally. In India, it remains largely untested at scale. That is the opportunity.

Revenue Models: What Exists, What Is Emerging, What Is Missing

| Model | Status in India | Lesson for Other Markets |

| Corporate Advertising | Dominant but weakening | Over-reliance creates editorial risk at any scale |

| Government Advertising | Significant for regional outlets; creates dependency | State funding needs firewalls — or creates capture |

| Digital Subscriptions | Under 2% penetration — huge untapped upside | Price is not the barrier. Habit and trust are |

| Membership / Donations | Working for some digital-first independents | Community before content is the key sequence |

| Events / Community | Emerging; underleveraged at regional level | Non-news revenue can fund news journalism |

| Regional Language Paywall | Almost entirely absent; early tests underway | Biggest untested opportunity in Indian media |

Based on FICCI-EY 2024, EY Media Report 2023, PwC India 2024, Reuters Institute 2024, and industry analysis.

What Other Markets Can Learn From India

The usual direction of learning runs the other way. India looks to Scandinavia for subscription models, to the US for digital innovation, to the UK for public media funding structures. That is reasonable. But there are things India’s situation reveals that other markets should pay attention to.

First: advertising dependency is a slow poison, not a sudden collapse. India’s crisis has been building for decades. The habit of making news free and funding it through advertising created a reader base that sees no reason to pay, and an advertising market that can hold journalism to account in ways that have nothing to do with editorial quality. Markets that are still advertising-dependent, including many local and regional outlets in the US and Europe, should read India as a preview of where that road leads.

Second: language is a business model question, not just an editorial one. The markets with the strongest reader revenue tend to be linguistically specific: Norwegian papers serving Norwegian readers, Finnish outlets serving Finnish readers. The intimacy of language creates the trust that makes people pay. Outlets that speak to readers in their own language, on their own terms, about their own communities, have a structural advantage in building paying audiences. That lesson travels.

Third: the path to reader revenue runs through habit, not price. India is not a poor market in the way the affordability argument implies. It is a market where the habit of paying for news was never built. Building that habit requires patience, consistency, and genuine editorial independence. It cannot be rushed by a paywall alone. Markets that are trying to pivot quickly from advertising to subscriptions are discovering the same thing.

Closing

India’s local news problem is not unique. It is the global local news problem at a scale and speed that makes the dynamics visible earlier and more sharply than elsewhere. The advertising model is weakening. Subscription habits have not been built. Government dependency creates editorial risk. Regional and vernacular journalism is structurally underinvested.

The question is not whether this will resolve itself. It will not. The question is whether the journalism and policy community acts on what India’s situation already makes plain, before other markets arrive at the same place with fewer options left.

Rudra Kasturi is a founder, investor, and strategy advisor who has worked across India’s largest media and technology companies, and who currently coaches CEOs and leadership teams, teaches AI, and helps companies scale in growing markets.

Share